What is the bond market outlook?

Longer-dated Bonds – Stick or Twist?

Friday 17 November, 2023

-

Government bonds can be considered in two dimensions – the ongoing coupon-based return associated with their ‘yield’ and the potential gain or loss associated with their price rising and falling, the magnitude of which is related to their interest rate sensitivity, or ‘duration’.

-

Times have moved on from the ‘return-free risk’ which mid and longer-dated UK government bonds arguably offered investors two to three years ago, with these investments now offering higher levels of yield.

-

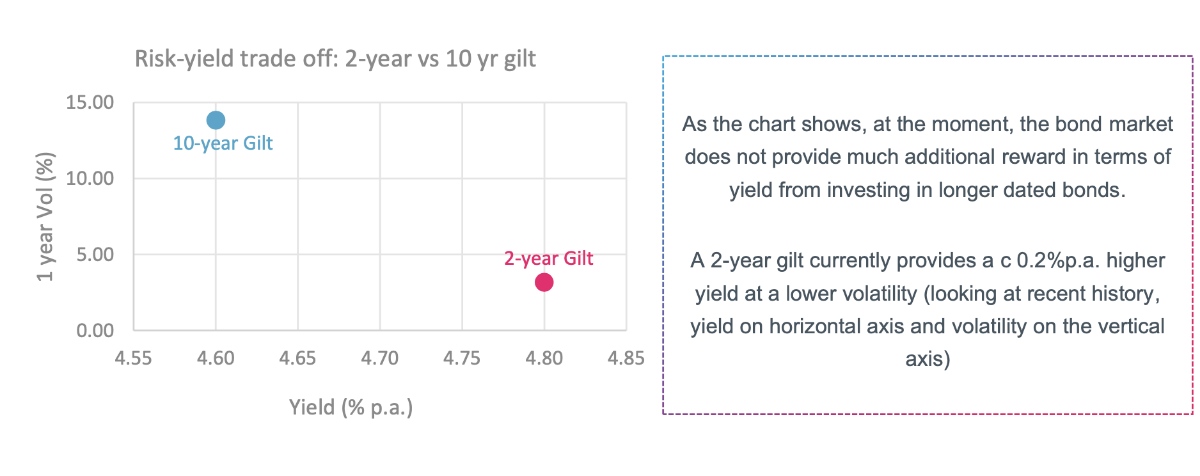

However, our sense is that, for the moment, bond-oriented portfolios should continue to have a bias towards shorter-dated bonds. At this time, these offer higher ongoing yields, at lower levels of volatility than their longer-dated peers making them an attractive investment for lower risk investors.

The recent history of the bond market

Bond markets have experienced heightened volatility and a significant sell-off in recent years. From individual investors' perspective, this has been most felt by those invested in ‘lower risk’ multi-asset portfolios, not least because these portfolios do not typically make material portfolio allocations to equities – which have fared better.

To give a measure of the severity of the bond market down-turn - two of the most followed market indices, the FTSE Gilts All Stocks and the FTSE Index-linked Gilts All Stocks, have returned -25% and -35% respectively over the past two years.

A number of active multi-asset portfolio managers (HRIS included) have helped protect investors from the worst of the sell-off in bonds over this time, through careful management of the interest rate sensitivity (sometimes referred to as ‘duration’). Whilst not immune to the sell-off, shorter duration UK bonds have fared relatively better – for context, the FTSE All Gilts under 5 years has returned -3.9% over the same time frame.

However, many investors, particularly those adopting a traditional, entirely ‘passive’ approach to asset allocation have been hit hard. This is because these strategies tend to hold longer-dated government bonds on an ongoing basis as a matter of course, irrespective of the short-and-medium term outlook for the bonds.

Irrespective of success or failure in navigating the bond markets to-date, advisers overseeing multi-asset portfolios may be wondering what their options are, and how to best advise clients in relation to their portfolio options, as we look ahead.

Understanding the outlook for bonds

The first step in understanding the current outlook for bonds involves looking at the risk and reward trade-off that investors currently face.

The ‘silver lining’ in relation to the recent sell-off in government bonds is that they now offer much more attractive levels of ongoing yield. For example, a 2-year UK Gilt currently offers investors 4.8%p.a. yield – a material increase from 0.4% in October 2021. Consequently, most multi-asset investors now see a valuable role for fixed income investments in portfolios – as a helpful means of gaining returns without facing some of the risks inherent to equities and other asset classes.

However, this is just part of the story. Consideration should also be given to the term of bond investments i.e. are return prospects equally attractive across different time frames, a 2-year gilt versus a 10-year gilt for instance; as well as any concerns over re-investment risk i.e. the rate at which short-dated bonds can be reinvested in the future. And, taking these factors into account, whether investors should look to alter the duration of bond holdings, potentially to increase yield, but more critically to increase the potential for price gain or loss in the investment?

Legacy longer-dated bond portfolio exposures - hold-on and hope for a recovery, or make a change?

In reality, the most appropriate course of action will depend on the specific client circumstance, including the time horizons of the end investors. However, in general terms we would note that:

-

Long-dated gilts and index-linked bonds will likely remain volatile for some time to come – due to ongoing uncertainty related to inflation, central banks and policy maker’s monetary policy responses and the impact of QT programmes;

-

Bond markets can be considered “efficient” markets meaning today’s bond prices have already ‘priced in’ an assumed path of future interest rates. Consequently, it is worth noting that, in most developed markets (including the UK), bond prices already account for a pausing and eventual reduction in long-term interest rates (of course expectations are subject to change as they have done in the past, but at present markets and central banks views appear relatively aligned).

It feels extremely unlikely that longer-dated bonds will recover a significant proportion of their prior ‘lost ground’ in the coming months, possibly years, with returns likely to largely come from coupons, rather than significant price appreciation. This is because we are likely to remain in a higher interest environment for some time – think “Table Mountain not Matterhorn” in the words of Bank of England’s Chief Economist Huw Pill. The probability of returning to a low yield environment (e.g. rates of 3% or less) feels low – with a corresponding lack of potential for bond price appreciation.

Looking ahead, flexibility remains key. The rationale for holding longer-dated government bonds (including alternative geographies) will evolve and, in our view, managing the exposures effectively will call for an active approach to active asset allocation, as opposed to simply holding onto a long-term passive allocation to specific bonds.

Risk warning

This communication is issued and approved by Hymans Robertson Investment Services LLP. It is based on its understanding of events at the time of the relevant preparation and analysis. The information and opinions contained in this document are provided by HRIS and are subject to change without notice and should not be relied upon when making investment decisions. The value of your investments and the income from them may go down as well as up and neither is guaranteed. Investors could get back less than they invested. Past performance is not a reliable indicator of future results. Changes in exchange rates may have an adverse effect on the value of an investment. Changes in interest rates may also impact the value of fixed income investments. The value of your investment may be impacted if the issuers of underlying fixed income holdings default, or market perceptions of their credit risk change. There are additional risks associated with investments in emerging or developing markets. The information in this document does not constitute advice, nor a recommendation, and investment decisions should not be made on the basis of it. The material provided should not be released or otherwise disclosed to any third party without prior consent from HRIS.

Latest News Next Article Previous Article