Sustainable Investing: Our views on the E, the S and the G

Tuesday 6 September, 2022

The integration of three words; is it supposed to save the planet?

ESG attracts its fair share of skeptics with recent reports claiming the integration of Environmental, Social and Governance in company analysis is often ‘well-meaning but deeply flawed’(1).

Whilst such reports acknowledge that increasing numbers of people want to manage their investments in line with their values, they criticise the ESG movement for being too complex, full of hidden incentives and burdened by a measurement problem.

In this thought piece, we take a deeper dive into these views and share our perspective.

The importance of the E, S and G

Climate change is a crucial issue facing us today, and we agree that prioritising emissions helps to focus investor attention and action in terms of the environment. It is also widely understood, there needs to be a stronger role played by corporates and governments in the transition to a low carbon economy. However, with high levels of inflation, energy costs rising and the human impact of both climate change and tackling it, it would be remiss to exclude the S, in terms of how companies interact with their employees and the communities in which they operate. Finally, removing the G lens leaves us exposed to too many risks, one example being financial fraud - anyone remember Enron?

Seemingly, ESG has been branded as a solution to a problem it never attempted to solve. Using E, S and G factors to analyse company risks and channel funds into companies with better sustainable profiles than their peers, results in boosting the share price of companies scoring well on these internal comparative metrics. It also potentially avoids some unpriced risks. ESG needs to be considered as an additional lens to view the inner workings of a business but is certainly only one part of the puzzle when it comes to the complexity of investing sustainably.

What are the claims and where do we stand?

1. ESG is too complex, it should only be E for Emissions:

Claim: using ESG distracts from the vital task of tackling climate change, instead investors should focus just on the E for environmental. And in fact, the E should be rebranded to Emissions alone.

View: we agree the focus on emissions needs to remain and decarbonisation rates need to accelerate. This is why we look at carbon metrics for all funds and companies, measuring both the absolute emissions but also carbon avoided. Our belief, that carbon is not yet fully priced in by markets has led us to review forward looking metrics like a net-zero transition score card for companies. This looks at implied temperature rise metrics, as well as companies’ committed targets and their verification via the Science Based Targets Initiative.

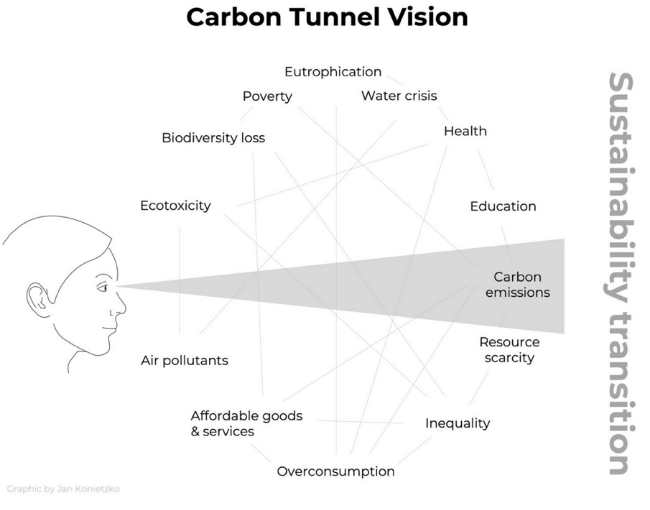

It is, however, important to not disregard other environmental factors like biodiversity, water scarcity or air quality when it comes to the E in ESG. This ‘carbon tunnel vision’ problem, underestimates the interlinked nature of ESG. Focusing on carbon as the only metric ignores both health impacts of fossil fuels and the just (people) transition that is necessary to move away from oil and gas. Whilst one metric may help simplify measurement, under a carbon lens it may seem like the best solution is to direct all capital to towards wind farms, however, this could end up destroying natural habitats, reducing biodiversity through construction, and encouraging slave labour in the mining sector that provides the rare earth components for the wind turbine technology.

2. There are too many hidden incentives

Claim: the quick move many providers have made into offering sustainable solutions is a display of an asset gathering exercise and not a genuine commitment to ESG or sustainable investing.

View: although it’s no surprise that asset managers are being quick to create or rebrand products to keep up with demand, achieving the sustainable development goals requires additional funding of $5-7 trillion, hence we believe the private sector has a pivotal role to play. Market forces have been active in some asset class markets driving change through the issuance of new instruments to tackle environmental and social challenges. Credit markets are a good example: investor demand for non-traditional bonds has grown and the number of green and sustainability linked bonds has boomed.

We acknowledge that there are discrepancies in quality between the types of bonds being issued, however, the market positioning towards sustainability is clear. We also continue to see a large difference in the credibility of sustainable investment style and disclosures among third party fund managers. Whilst regulation such as the EU’s Sustainable Finance Disclosure Regulation (SFDR), the UK’s FCA planning to release their Sustainable Disclosure Requirements (SDR) in September, and the US Securities and Exchange Commission (SEC) fund naming rule under consultation, all attempts to help distinguish between funds. Although investors will need to look beyond labels, understanding the fund’s holdings and the fund manager’s rationale for why certain companies make it into a sustainable fund. We spend a lot of time vetting sustainable funds at LGT Wealth Management, as we focus on intentionality, understanding the manager’s policies and processes to ensure sustainability and ESG is truly integrated and not just part of an asset gathering exercise.

3. ESG is too hard to measure and quantify

Claim: ESG scoring systems have a huge amount of inconsistencies. Credit ratings have 90% correlation across rating agencies, however ESG ratings tally little more than half the time.

View: divergence and variety allow us to have a stronger set of measures, and create our own sophisticated framework, which we can both understand and defend. We do not take an overly manufactured ESG score, but rather we find the variety in underlying indicators a richness that allows us to add complexity and detail to our interpretations of companies’ ESG performance. Using various data points that are material to different industries or sectors provide us the opportunity to reflect on the diverse challenges faced by different industries, as a one size fits all approach doesn’t capture the subtleties needed for robust ESG analysis.

Having our own tool and methodology means we can be more flexible and agile when trends or new data emerges, such as incorporating biodiversity metrics into our scoring. Importantly, quantitative scores are just a starting point in our analysis, and not the basis on which we would invest our sustainable clients’ money. We review qualitative data, controversies, engagement results and of course financial performance to build a well-rounded picture.

Considering all perspectives

As many investors who are now well versed in the art of sustainable investing would agree, the recent criticisms of ESG are not new. These concerns are valid and it’s important to both hear and consider them. Ultimately, we believe it’s important to acknowledge all of the benefits and developments considering ESG characteristics have led to. It’s equally important to challenge processes and ensure the sustainable investing community continues to evolve. In the process of doing so, we may just help to save the planet.

1. https://www.economist.com/leaders/2022/07/21/esg-should-be-boiled-down-to-one-simple-measure-emissions

Important information

This document is for informational purposes only and should not be construed as advice or an offer, invitation or solicitation to enter into any financial obligation, activity or promotion of any kind. Past performance is not an indication of future performance, capital is at risk and the value of investments and the income derived from them may fluctuate and may be affected by exchange rate variations. The information and opinions expressed herein are the views of LGT Wealth Management UK LLP and are based on current public information we believe to be reliable but we do not represent that they are accurate or complete and should not be relied upon as such. Any information herein is given in good faith, but is subject to change without notice. No liability is accepted whatsoever by LGT Wealth Management UK LLP, employees and associated companies for any direct or consequential loss arising from this document. This document is not for distribution outside the United Kingdom.

Investors should be aware that past performance is not an indication of future performance, the value of investments and the income derived from them may fluctuate and you may not receive back the amount you originally invested.

Latest News Next Article Previous Article