UK Markets Review

Update on UK Markets

Wednesday 28 September, 2022

Update on UK Markets provided with the assistance of Hymans Robertson.

- On 23 September the newly appointed Chancellor announced a spate of tax cuts, funded through additional Government borrowing triggering a wave of selling in UK assets

- The pound weakened sharply following the announcement, reaching as low as $1.03 against the US dollar the following Monday (26 September)

- UK government bonds (gilts) fell in value as yields rose significantly; but while UK equities also fell, the weaker pound helped investors in overseas assets

Why are gilts selling off?

The energy price guarantee support to households and businesses, alongside permanent tax cuts, will likely lead to a marked deterioration in public finances from October, when the energy support package takes effect. Indeed, the Institute for Fiscal Studies and Citi have said the budget risks putting the UK public finances on an unsustainable path. The cost of the energy support package is unknown as it will depend upon volatile gas prices,but external estimates have placed the bill as high as £150bn. As the government embarks on tax cuts, the cost will need to be met by additional borrowing, and so the deteriorating fiscal position should lead to an increase in the supply of government bonds.

We expect the budget will deliver a short-term boost to demand, potentially lessening the depth of the current growth slowdown. However, it remains to be seen whether suggested tax cuts, promised deregulation and indeed the new real growth target, will do much to alter the longer-term growth outlook.

The impact on inflation

The government intervention on energy prices is likely to limit the near-term peak in energy prices but the fiscal loosening is likely to support aggregate demand at a time of existing high inflation and generate greater medium-term inflation pressure than would otherwise have been the case. As a result, the Bank of England (BoE) are unlikely to shift from their hawkish stance of rate hiking and the recent fiscal developments may even lead to greater monetary tightening for a longer period than was previously envisaged, despite the actual headline rate peaking at a lower level (now anticipated to peak around 11% year-on-year in October).

This, and the additional issuance required to fund large fiscal intervention could place ongoing upwards pressure on gilt yields in the near-term. At the same time, the Bank of England is expected to begin quantitative tightening (i.e. active gilt sales) at the end of September. This has been well telegraphed to the market but is yet one more near-term technical headwind for gilt markets. In concert, greater issuance, medium-term inflation concerns, and gilt sales are likely to place further near-term upwards pressure on interest rate expectations and yields. On the morning of Monday 26 September, markets started to heavily price in a rate hike over the following week at an emergency meeting, although the BoE seemed to rule this out in a statement released later that afternoon. A significant rate hike is now expected at the next scheduled meeting in November and at later meetings with Overnight Index Swaps suggesting UK rates will exceed 6% p.a. by next May. We anticipate further volatility and potentially further upwards pressure on longer-term yields.

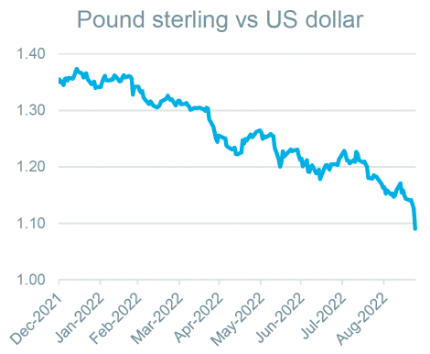

Why has sterling weakened so much?

Sterling has weakened materially this year, most significantly against the dollar where it has fallen by around 20% (see chart), as the economic outlook has deteriorated. Sterling took yet another leg lower upon Liz Truss winning the Conservative leadership contest and the release of early details of her energy support package, deregulation and tax-cutting agenda. On Friday, as the tax cuts were announced, the sell-off accelerated. An upgrade in expectations of interest rates is normally accompanied by a strengthening currency, the fact that the pound has weakened at the same time as higher interest rate expectations points to concerns around the medium-term growth and inflation outlook as opposed to reflecting an expectation of a higher real growth target being realised.

A poor UK economic outlook may not spell disaster for investors

2022 has so far been a chastening year for bond investors and the latest week would have been a tough one for gilt holders. Investors, such as ourselves, that have held shorter dated bonds would have been partially protected owing to their reduced sensitivity to increases in yield. Although we expect volatility to remain in the bond market, yields have increased across the maturity curve and are now more attractive than where they were earlier in the year.

Sterling weakness year-to-date has enhanced overseas returns to unhedged sterling-based investors. Global equity markets were down 19.5% in the year to 23 September. However, when accounting for changes in currencies, sterling-based investors are down just 4.9%. This dynamic has once again helped investors in the past week and reiterated our long-held belief in the value of a globally diversified portfolio, especially in times of market stress. While sterling looks cheap relative to measures of fair value, it is difficult to see a near-term catalyst to support a stronger sterling.

Risk warning

This communication is issued and approved by Lonsdale Services Ltd. It is based on its understanding of events atthe time of the relevant preparation and analysis. The information and opinions contained in this document are provided by Lonsdale and are subject to change without notice and should not be relied upon when making investment decisions. The value of your investments and the income from them may go down as well as up and neither is guaranteed. Investors could get back less than they invested. Past performance is not a reliable indicator of future results. Changes in exchange rates may have an adverse effect on the value of an investment. Changes in interest rates may also impact the value of fixed income investments. The value of your investment may be impacted if the issuers of underlying fixed income holdings default, or market perceptions of their credit risk change.

There are additional risks associated with investments in emerging or developing markets. The information in this document does not constitute advice, nor a recommendation, and investment decisions should not be made on the basis of it. The material provided should not be released or otherwise disclosed to any third party without prior consent from Lonsdale.