The AI Bubble: Turn Market Fear into Investment Focus

Tuesday 25 November, 2025

In recent months, many clients have been asking the same questions:

“Are we in another financial markets bubble?”

“Should I be investing right now and, if so, what should I invest in?”

“Should I be selling shares while financial markets are at all-time highs?”

These questions are entirely natural. After three strong years of returns, the familiar chorus of “financial experts” has returned, warning of crashes, bubbles, and sudden market downturns. Headlines shout of an AI bubble, and online commentators proclaim that a market crash is coming. These are the same recycled warnings investors have heard for decades.

Market history is full of predictions that never quite materialise, yet we find ourselves listening every time. The current warnings about AI feel reminiscent of those heard during the dot-com boom of the late 1990s. And yes, those warnings proved correct eventually.

But many investors who acted too early missed years of growth and were scared out of owning some of today’s most successful companies.

Market Corrections Are Normal, Recovery is the Rule

It helps to put these concerns into perspective. Since 1986, the UK’s FTSE 100 has experienced 22 market corrections of greater than 10%. A correction, a fall of 10–20% from a recent high is a common part of market cycles, whereas a bear market is typically defined as a decline of 20% or more. Understanding this distinction is important for any long-term investor.

Historical data also show that financial markets tend to recover. After a decline of more than 10%, the FTSE 100 has taken on average around 336 days to recover to previous highs. While “on average” is not “immediate,” it highlights that patience and discipline are vital.

Over longer periods, UK equities have delivered average annual returns of around 6%–6.6%, much of which came from reinvested dividends. Even though volatility is inevitable, the long-term reward generally favours those who remain invested.

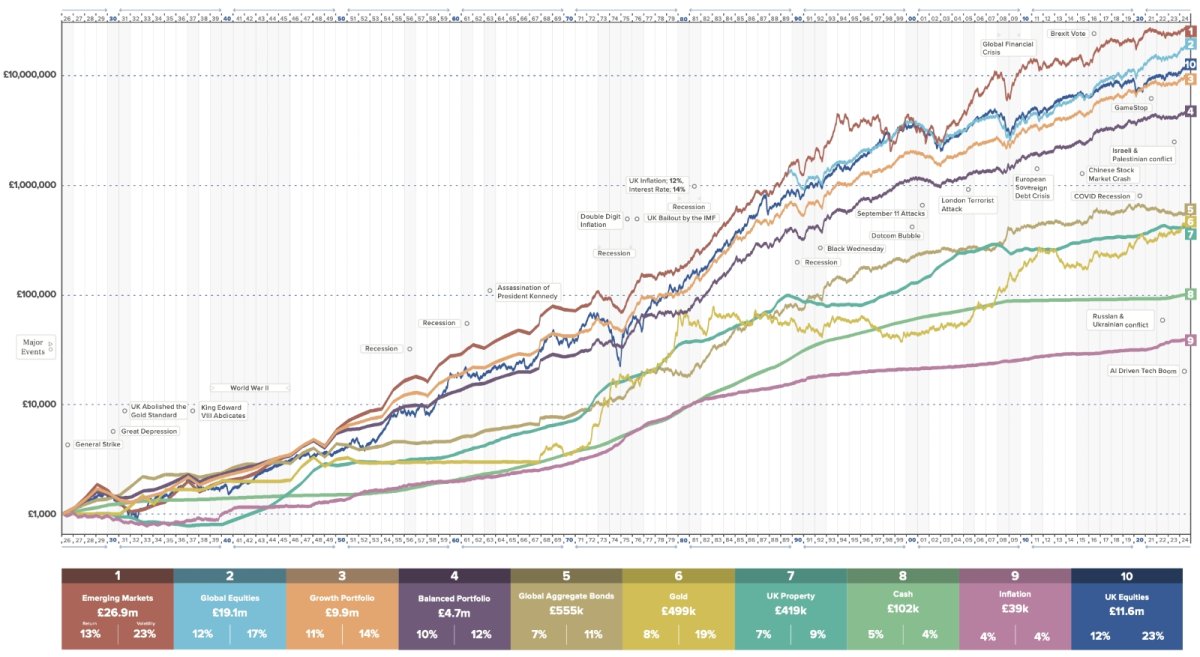

Growth of Wealth**

This chart shows the inferred growth of money invested on January 1st, 1926.

The Real Investment Risk Lies in Reaction

Market declines are inevitable, but the greater risk is reacting to them emotionally. Investors who sell at the first sign of trouble often lock in losses and miss the recovery that follows.

Markets move in cycles, not straight lines, and one impulsive decision can undo years of steady progress. Rebuilding confidence after a hasty choice is far harder than maintaining discipline through temporary declines.

Market Investments: Fix the Roof While the Sun is Shining

This brings us back to timeless wisdom: “Fix the roof while the sun is shining.”

Now is the time to make sure your financial foundations are secure. Ensure your plans do not rely on timing the market. Focus instead on ownership, clarity of purpose, and disciplined investing.

At Lonsdale Wealth Management, our financial advisers help clients turn uncertainty into confidence. We build financial plans and investment strategies designed to give your money a purpose, to support your life, your goals, and your future.

Our financial advisers understand risk: when to take it, how to manage it, and how to use it to improve long-term outcomes. We also ensure that our clients understand the risks they are taking and, importantly, why they are taking them.

Conor McClean, Independent Financial Adviser (IFA) in St Albans said:

“Financial planning is not about reacting to headlines. It’s about creating strategies that withstand the ups and downs of markets, designed to help you achieve your goals no matter the economic cycle. By staying disciplined, focused, and confident, you can ensure that when the clouds of market uncertainty inevitably arrive, your financial roof is already strong and secure.”

Speak to a Local Financial Adviser

If recent headlines have left you feeling unsure about your portfolio, your pension, or the path ahead, now is the time for a conversation, not a reaction. Whether you’re questioning your current investment strategy, wondering if your risk level is appropriate, or simply want clarity and confidence in the decisions you’re making, we’re here to help. Get in touch with Lonsdale Wealth Management for a no-obligation discussion and let our financial advisers help you turn uncertainty into clear direction, disciplined planning, and long-term confidence in your financial future. Call 01727 845500 or email enquiries@lonsdaleservices.co.uk to help to regain confidence.

Note: The value of an investment and the income from it can go down as well as up. The return at the end of the investment period is not guaranteed, and you may get back less than you originally invested. A pension is a long-term investment not normally accessible until age 55 (57 from April 2028 unless the plan has a protected pension age). The value of your investments (and any income from them) can go down as well as up which would have an impact on the level of pension benefits available. The contents of this article are for information purposes only and do not constitute individual financial advice.

Sources:

https://www.arbuthnotlatham.co.uk/insights/brief-history-market-corrections

https://www.ig.com/uk/trading-strategies/what-are-the-average-returns-of-the-ftse-100--230511

https://ifamagazine.com/ftse-100-celebrates-40th-birthday-but-is-it-over-the-hill

**Growth of Wealth Graph: Global Balanced Portfolio is made up of 50% Global Equities and 50% Global Bonds. Global Growth Portfolio is made up of 60% Global Equities, 10% Emerging Markets and 30% Global Bonds. This chart is for illustrative purposes only; it does not constitute investment advice and must not be relied on as such. The value of investments and the income from them can go down as well as up so you may get back less than you invest. Past performance is not a guide to what might happen in the future. Transaction costs, taxes and inflation reduce investment returns. This chart shows the inferred growth of money invested on January 1st, 1926. The return of each asset class is the average of calendar returns, and the volatility of each asset class is the standard deviation of the calendar returns. Major political and financial events are indicated by • and ►. The portfolios are hypothetical and are rebalanced annually on the 1st of January. All investment income is assumed to be reinvested, unless otherwise stated. No transaction costs or taxes are included. Sources: UK Equities: Timeline UK Equity TR Index: Bank of England: A Millennium of Macroeconomic Data and FTSE All Share TR, Global Equities: Morningstar Global All Cap Target Market Exposure Index, Emerging Markets Equities: Fama/French Emerging 5 factors Index, UK T Bills: UK One-Month Treasury Bills Index, Global Bonds: Morningstar Global Core Bond Index, Gold: Timothy Green's Historical Gold Price Table and World Bank Commodity Price Data, UK Property: Timeline UK Property house price Index: Bank of England: A Millennium of Macroeconomic Data and UK Nationwide House Pricing Data, UK Inflation: Headline Consumer Price Index via Bank of England: A Millennium of Macroeconomic Data and the ONS. Source: Timeline Limited using data from Morningstar. Copyright © 2025. Timeline Limited. All rights reserved.

Latest News Next Article Previous Article