The Hidden Inheritance Tax Cash-Flow Trap Facing High Net Worth Families

Wednesday 20 May, 2026

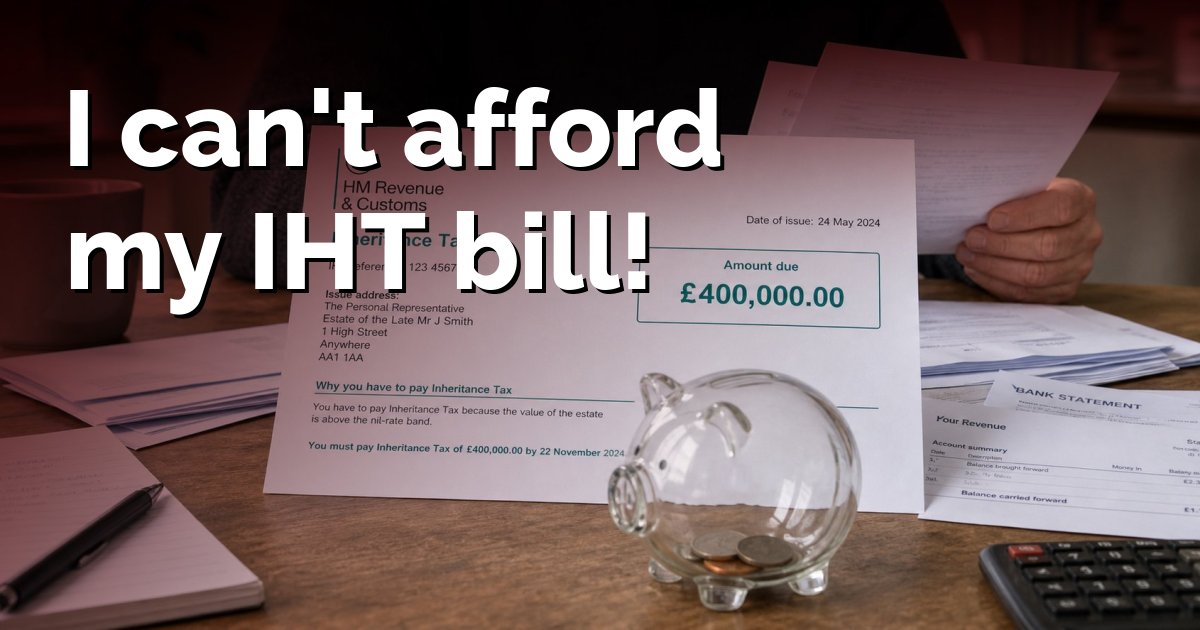

I can’t afford to pay a £400,000 inheritance tax bill because I haven't received my inheritance yet, what shall I do?

For many high-net-worth families, inheritance tax planning often focuses on reducing the eventual tax bill.

However, one of the biggest problems families may face is not always the amount of Inheritance Tax (IHT) due, but how quickly it has to be paid and where the money will come from.

It is a situation that can place enormous pressure on families at an already difficult and emotional time.

A £400,000 Tax Bill Before the Estate Can Be Accessed

For a married couple with an estate worth around £2 million, the inheritance tax position can be significant.

Even after applying two full Nil Rate Bands (NRB) of £325,000 each and two full Residence Nil Rate Bands (RNRB) of £175,000 each, the estimated inheritance tax bill could still be around £400,000.

To explain these allowances more clearly:

- The Nil Rate Band (NRB) is the amount of an estate that can be passed on free of inheritance tax. Each individual currently has an allowance of £325,000.

- The Residence Nil Rate Band (RNRB) is an additional allowance available when passing the family home to direct descendants, such as children or grandchildren. This allowance is currently £175,000 per person.

Anything above these available allowances may be subject to inheritance tax at 40%.

The Six-Month Inheritance Tax Deadline Many Families Do Not Expect

Inheritance tax on a UK estate normally has to be paid within six months of the end of the month in which the person died.

If the tax is not paid on time, HM Revenue & Customs (HMRC) can charge interest from the due date. Current late payment interest rates are 7.75%.

The difficulty is that executors often cannot easily access the estate funds needed to settle the bill.

Conor McClean, Independent Financial Adviser (IFA) in St Albans, Hertfordshire said:

“Many families focus entirely on the size of the inheritance tax bill, but the real issue is often how quickly that money is needed and whether it can actually be accessed in time. Proper financial advice and planning is about making sure the right structures and liquidity are in place, so loved ones are not placed under unnecessary financial pressure.”

Why The Six-Month Deadline Creates a Serious Cash-Flow Problem

Before executors can fully deal with an estate, they usually need to obtain a Grant of Probate. This is the legal document that gives them authority to access accounts, sell assets and administer the estate.

However, in many inheritance tax cases, HMRC expects the tax to be paid before probate is granted.

This creates a frustrating and stressful position for families because, without probate, they may not be able to:

- Access bank accounts held solely in the deceased’s name

- Sell property

- Release investments or other assets

- Distribute funds to beneficiaries

In simple terms, the money needed to pay the inheritance tax may effectively be locked inside the estate itself.

Delays Are Becoming Increasingly Common

For larger or more complicated estates, particularly those valued between £2 million and £3 million or more, the full administration process can now take between nine and twelve months from death to final distribution, and in some situations even longer.

Where business interests, multiple properties or more complex assets are involved, delays can increase further.

Currently, obtaining probate alone for a complex inheritance tax estate can take around sixteen to twenty weeks. If property then needs to be sold afterwards, families can face an even longer wait before funds become available.

Where Can the Money Come From?

Because the inheritance tax bill often needs to be paid before estate assets can be released, families may need alternative sources of liquidity.

Possible options can include:

Cash or Liquid Investments Within the Estate

If there is sufficient cash available in accessible accounts, this may help cover part or all of the inheritance tax liability.

Life Assurance Written in Trust

Life assurance policies written into trust can provide immediate funds outside the estate. Because the policy is held in trust, the payout can usually be made quickly to the chosen beneficiaries without waiting for probate.

Joint Accounts

Jointly held bank accounts may automatically pass to the surviving spouse or account holder, potentially providing immediate access to funds.

HMRC Instalment Arrangements

Under Section 227 of the Inheritance Tax Act 1984, inheritance tax relating to certain assets, such as property or qualifying business interests, may be paid in instalments over up to ten years. However, interest will still apply to outstanding balances.

New assets from 6 April 2026

For any new assets you inherit from 6 April 2026 onwards, instalments are interest-free if the asset qualifies for Agricultural Relief, or Business Relief. If you pay an instalment late, you’ll still need to pay interest from the date it’s due to the date of payment. You will not pay any interest on the outstanding tax balance. These rules do not apply to any assets you were already paying instalments on before 6 April 2026.

Probate Lending

Some families consider probate-secured lending against the estate. While this can provide short-term liquidity, it can also be an expensive option, and professional advice is important before proceeding.

Pension Changes Could Increase the Problem Further

The planned pension changes due from April 2027 are expected to make this inheritance tax cash-flow issue even more challenging for some families. These changes are substantial enough to warrant separate detailed consideration as part of wider estate and inheritance tax planning.

Planning the Cash Flow Is Just as Important as Planning the Tax

One of the biggest lessons for high-net-worth families is that inheritance tax planning should not focus solely on reducing the tax liability itself.

Families also need to consider:

- How the tax bill would actually be paid

- Whether sufficient liquidity exists

- How quickly funds could be accessed

- What happens if probate is delayed

- Whether protection arrangements are in place

Without proper planning, even asset-rich families can find themselves under significant financial pressure.

How Lonsdale Can Help

At Lonsdale, our financial advisers work closely with individuals and families to help structure inheritance tax and estate planning arrangements in a practical and tax-efficient way.

This includes reviewing potential inheritance tax exposure, assessing liquidity needs, considering trust and protection arrangements, and helping clients create long-term plans designed to reduce financial stress for loved ones.

Professional advice can make a considerable difference when it comes to preparing for the unexpected and ensuring families are not left facing avoidable complications during an already emotional period.

Please note: The contents of this article are for information purposes only and do not constitute individual financial or legal advice. The information contained within this article is based on our understanding of legislation, whether proposed or in force, and market practice at the time of writing. Levels, bases and reliefs from taxation may be subject to change. The Financial Conduct Authority does not regulate estate planning, tax advice, trusts and wills.

Latest News Next Article Previous Article